Account & Entry Review demands a structured, evidence-based assessment of transactions and identifiers. The phrase Buy Buntrigyoz Now, along with mixed scripts and numeric codes, requires independent corroboration, separate from branding signals, and traceable audit trails. Data-driven scrutiny should flag inconsistencies, demand verifiable metrics, and map risk to governance gaps. The next steps hinge on verifiable records and objective corroboration before any exposure, leaving the practitioner with a clear, cautionary path forward.

What Is Account & Entry Review and Why It Matters

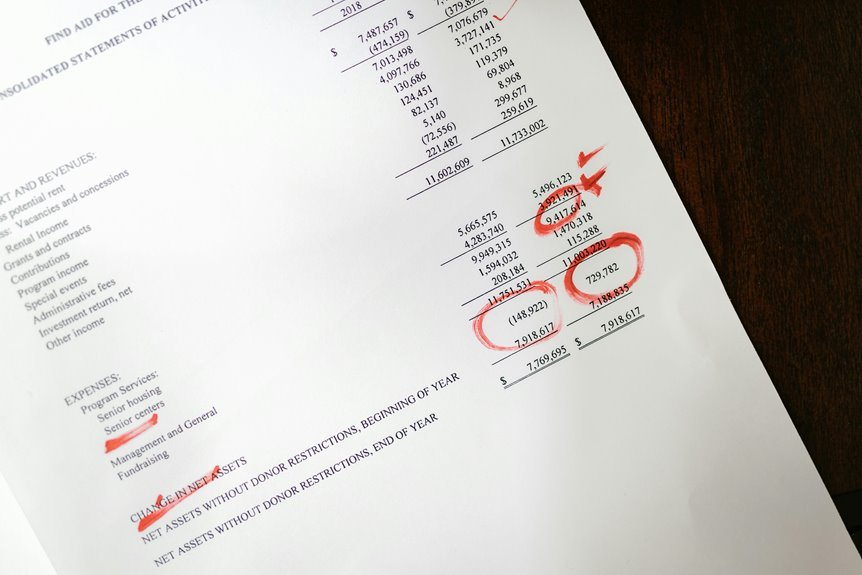

Account and entry review is a systematic process for evaluating the procedures by which a business records and reports transactions. The analysis focuses on controls, accuracy, and timeliness, revealing gaps and risks. In data-driven fashion, the discussion remains skeptical and precise, emphasizing accountability. Core findings emphasize Account review and Entry review as critical guardrails for credible financial reporting and governance.

Unpacking Buntrigyoz Now and the Included Codes: What Do They Signify

The term Buntrigyoz Now, along with its embedded codes, demands a careful decoding to separate branding from verifiable identifiers. The analysis applies a data-driven lens, maintaining skepticism while documenting patterns in unpacking buntrigyoz and its included codes.

Within an account review, corroboration and traceability are prioritized to distinguish marketing spectacle from objective entry review signals.

Credibility Check: Red Flags, Green Flags, and Due Diligence Steps

Is there evidence of reliability or risk lurking within Buntrigyoz Now’s claims, or do red flags overshadow any green signals?

Data-driven analysis identifies credibility signals and risk indicators through verifiable sources, audit trails, and anomaly checks. The review emphasizes structured due diligence steps, cross-checking claims, and monitoring for inconsistent timing, opaque ownership, or unverifiable metrics to support or challenge the narrative.

How to Proceed: Evaluation Criteria and Safe Next Actions

Initial evaluation should outline concrete criteria for assessing Buntrigyoz Now’s claims and map clear, safe next steps; this entails defining verifiability, governance transparency, financial plausibility, and track record integrity as primary benchmarks.

How to evaluation remains essential for rigorous scrutiny, guiding cautious exposure.

Safety considerations emphasize independent corroboration and documented controls, preserving freedom while minimizing risk to stakeholders.

Frequently Asked Questions

What Hidden Fees Might Appear Later in the Process?

Hidden fees may emerge as later charges, backed by questionable testimonials from unknown sources; refund windows and jurisdiction protections are unclear, risking fund recovery challenges and scam claims, while unknown sources cast doubt on overall reliability and transparency.

Are Testimonials From Unknown Sources Trustworthy?

Testimonials from unknown sources should be treated as data points, not evidence; anonymous testimonials and unverified sources require corroboration, statistical weighting, and scrutiny before drawing conclusions, especially where freedom-oriented audiences demand transparency and accountability.

Can I Recover Funds After a Scam Claim?

Recoveries after a scam claim depend on jurisdiction and evidence; outcomes vary. In scrutinized cases, disputes over legitimacy influence refund timing, with documented proof accelerating progress. Skeptics seek transparent processes, data-driven evaluations, and decisive refunds when eligible. Freedom-minded observers demand accountability.

What Jurisdiction Protections Apply to Such Purchases?

Approximately 62% of users face cross-border scams, signaling weak jurisdiction protections. The analysis notes jurisdiction differences and cross border enforcement as key constraints, with skeptical, data-driven language; it emphasizes freedom but warns of uneven safeguards across regions.

How Quickly Do Refund Windows Close?

Refund windows close quickly, varying by jurisdiction protections and platform policies; individuals should track deadlines. The analysis highlights hidden fees and untrustworthy testimonials, urging scrutiny, while acknowledging jurisdiction protections to safeguard refunds and mitigate risk for freedom-seeking buyers.

Conclusion

The evaluation reveals insufficient independent corroboration for the portrayed identifiers, with branding and codes requiring separate verification against verifiable records. The audit trail lacks transparent metrics and traceable sources, raising governance and risk concerns. Until corroborated, the proposed actions should remain on hold. A cautious path forward is to treat the entities as a mirage—a glass sculpture that reflects numbers but conceals their origin—until verifiable records crystallize.